To understand autocallable ETFs, it’s helpful to start with the building blocks: autocallable notes.

What Are Autocallable Notes?

An autocallable note is a type of structured note that links coupon payments to the performance of a reference asset, typically an equity index, through embedded option structures.

At its core, an autocallable note pays a coupon if the reference index remains above a predetermined threshold. In exchange for that income potential, investors accept the risk that a severe and sustained market decline could interrupt payments or even result in principal loss.

The issuer establishes the structure at inception. Key terms typically include:

A reference index

A fixed maturity (often five years)

A coupon barrier

A principal barrier at maturity

A one-year non-call period (i.e., the initial period during which the note cannot be redeemed early)

An autocall level that can trigger early redemption (often one year)

After the non-call period ends, scheduled observation dates—often monthly—determine whether the position continues or redeems. If the reference index is at or above its starting level, the position may be called early and principal returned. If not, it continues until the next observation date.

Income is conditional. If the reference index remains above the coupon barrier at an observation date, the terms provide for a coupon payment. If it falls below that barrier, payments may pause. At maturity, the maturity barrier determines principal treatment. If the barrier isn’t breached, principal is returned in full. If it is breached, losses may occur in proportion to the decline. Advisors should understand that the note is subject to the credit risk of the issuer, and coupon payments are in no way guaranteed.

The structure involves defined tradeoffs: autocallable notes seek bond-like income derived from equity markets, in exchange for defined equity tail risk.

Why Autocallable ETFs Were Created

While autocallable ETFs seek to deliver similar income mechanics, it’s important to note that they are structurally distinct from autocallable notes. Autocallable structures have traditionally been accessed through structured notes.1 While these instruments have grown in popularity, accessing them has often involved operational considerations such as:

Large minimum investments

Limited liquidity

Individual note monitoring

Manual reinvestment when called

Potential tax complexity

An autocallable ETF may provide an alternative approach. From a structural perspective, an ETF can aggregate exposure across multiple structured positions with different entry points and timing, while providing daily liquidity and standardized reporting.

For advisors, this shift in format can also matter operationally. Rather than tracking individual note maturities, observation schedules, and issuer exposure across portfolios, the ETF structure centralizes that complexity within the fund itself, potentially making autocallable mechanics more accessible.

How Autocallable ETFs Work

Autocallable ETFs provide exposure to similar coupon and principal barrier mechanics described above, but within an exchange-traded structure, and with other important distinctions, characteristics, and risks.

Rather than holding autocallable notes directly, the ETF typically gains exposure to autocallable payoff mechanics through total return swap agreements that reference a rules-based index of synthetic autocallable yield notes. For purposes of brevity, and here only. we will call these “synthetic autocallables.” That index represents a portfolio of autocallables, each structured with consistent parameters: a defined maturity, a non-call period, scheduled observation dates, and defined coupon and principal barriers. Because the ETF uses synthetic autocallables rather than direct note ownership, investors may be exposed to additional complexities. That is to say: Autocallable ETFs are a novel and complex strategy, and advisors should make sure they review all terms carefully, which we outline below.

The ETF typically references a transparent, rules-based index that standardizes contract terms and systematizes issuance, ensuring that contract creation, observation schedules, valuation, and reinvestment follow predefined methodology.

The same barrier and observation logic applies across the portfolio’s synthetic autocallable exposures. After the non-call period, the index framework evaluates positions at regular intervals. Positions that meet the autocall conditions may be removed from the index and replaced, simulating an early redemption consistent with autocallable note mechanics. If not called, they remain outstanding and continue to be evaluated monthly.

The ETF's income reflects the aggregate returns from its swap agreements (i.e., the synthetic autocallable underliers), which are structured to pay conditionally based on whether the reference index remains above defined coupon barriers at each observation date. If the index falls below that threshold, payments pause for the affected positions and may resume if the index recovers above the barrier. At maturity, the principal barrier determines capital outcomes, consistent with the structured note mechanics described earlier.

Footnotes

For institutional, educational use only. The graphic presented herein illustrates a hypothetical autocallable structured investment payoff profile and is provided to explain the general mechanics of an autocallable strategy. The ETF referenced seeks to provide exposure to a transparent, rules-based index designed to replicate certain features commonly found in autocallable structured notes, including predefined observation schedules, barrier levels, valuation mechanics, and systematic reinvestment methodology.

The outcomes shown are hypothetical and do not represent actual investment results. Hypothetical illustrations have inherent limitations, are based on assumptions that may not prove to be accurate, and do not reflect actual trading, fees, expenses, taxes, liquidity constraints, counterparty exposures, or market conditions. No representation is being made that any investment will achieve results similar to those depicted.

CAIS and its affiliates are not fiduciaries and do not provide investment, legal, or tax advice. CAIS may receive compensation in connection with products made available through its platform. All investments involve risk, including the possible loss of principal. Investors should review the ETF’s prospectus, including its index methodology, risks, and expenses, and consult their legal, tax, and financial advisors before making any investment decision.

This communication is provided for informational purposes only and is intended solely for institutional investors and financial professionals. It is not intended for retail investors and does not constitute an offer to sell or the solicitation of an offer to buy any security or investment product. Any such offer may only be made pursuant to the applicable prospectus and offering documents.

Past performance is not indicative of future results.

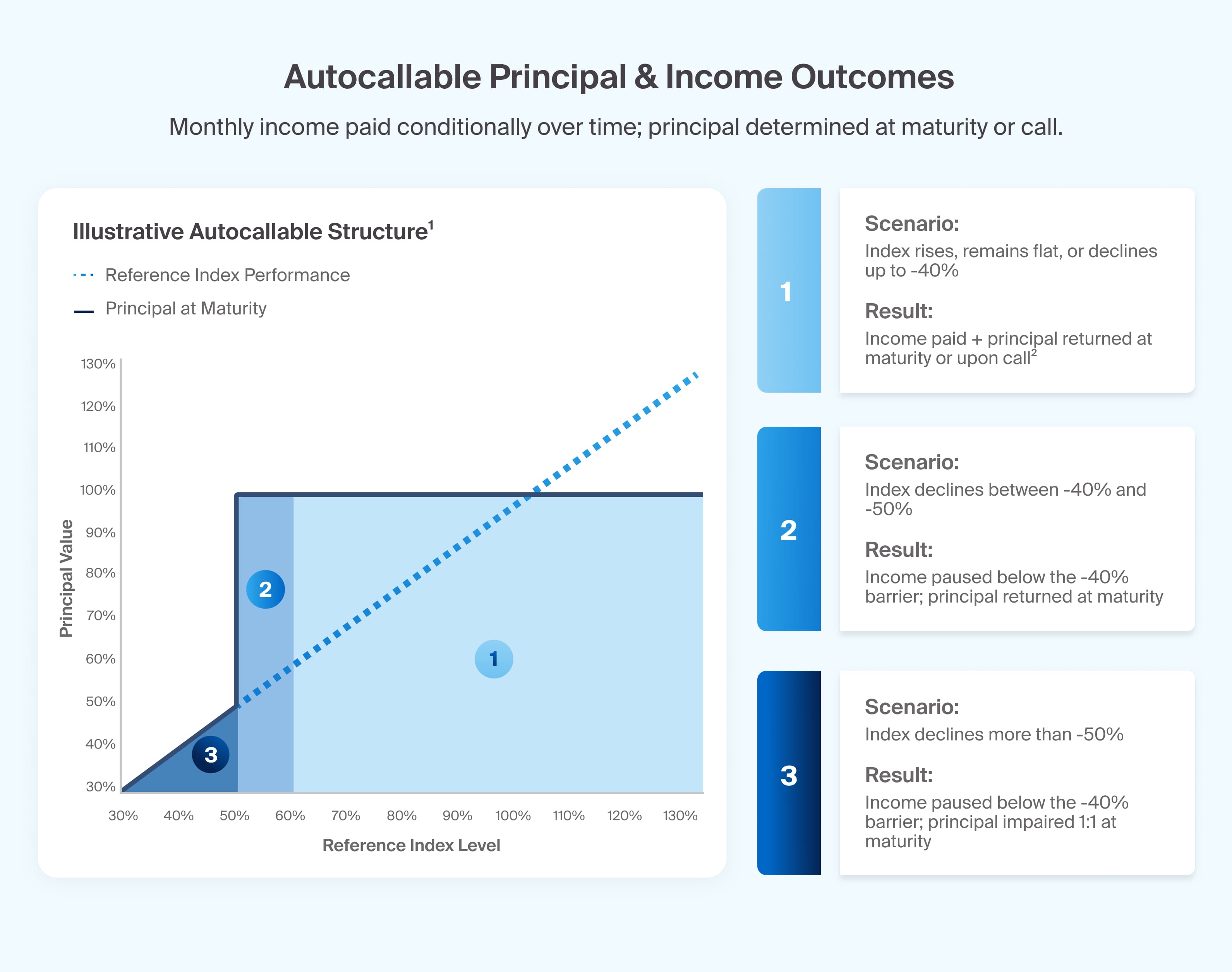

Autocallable payoff outcomes depend on where the underlier lands relative to predefined barrier levels (Exhibit 1)

Although individual positions define principal outcomes at maturity, the ETF itself trades daily on an exchange. The market price of ETF shares may differ from the fund’s net asset value (NAV), which is calculated based on the fair value of the underlying swap positions. Investors can buy or sell shares throughout the trading day, even though the underlying autocallable positions have defined lifecycles—and they’ll be transacting at market price, not NAV.

In rising or stable markets, many positions may be called shortly after the non-call period ends. When that happens, capital returns to the portfolio and may be invested into new positions with current market terms.

In moderately declining markets—where the reference index remains above the coupon barrier—coupon payments may continue even if overall equity returns are muted.

In more severe downturns, coupon payments may pause, and if the principal barrier is breached at maturity, losses may occur.

Because observation dates are often monthly, timing matters at the individual exposure level. Two investors entering the same autocallable note at different times may experience different outcomes depending on when market drawdowns occur relative to observation dates. But within an ETF, exposure may span many positions entered at different times. This is designed to reduce reliance on a single market entry point.

Key Characteristics of Autocallable ETFs

As we’ve discussed, autocallable ETFs seek to provide equity-linked, conditional income by gaining exposure to autocallable payoff mechanics through a diversified, rules-based portfolio of synthetic autocallables—not through direct ownership of autocallable notes—which changes how these mechanics are delivered and managed.

Conditional, Equity-Linked Income

Because the ETF has autocallable exposures entered at different points in time, income reflects the aggregate outcome of many observation cycles rather than a single binary event. However, distributions are not guaranteed and may vary across market environments.

Daily Pricing and Fair Value Exposure

Although individual autocallables define principal outcomes at maturity, an ETF is priced daily. The ETF’s NAV fluctuates with changes in the reference index, volatility, time to maturity, and proximity to barriers, even if the barriers are ultimately not breached. The market price at which investors buy or sell shares may differ from NAV depending on intraday supply and demand, and both may vary meaningfully in the short term.

Laddered Construction and Reduced Entry Concentration

Autocallable ETFs typically maintain exposure to synthetic autocallables entered at different points in time. This laddered approach reduces reliance on a single market entry or observation schedule and distributes exposure across entry points. While this structure may mitigate single-entry timing risk, it does not eliminate market risk or prevent losses in severe downturns.

Systematic Early Redemption and Reinvestment

When underlying positions are called after the non-call period, capital is redeployed according to the index methodology. This removes the operational burden of reinvesting individual notes and maintains continuous exposure. However, prevailing market conditions at the time of reinvestment may affect the terms available for newly entered contracts.

General Risks and Considerations of Autocallable ETFs

Complexity and Volatility Sensitivity: The conditional nature requires ongoing attention to understand scenario-specific outcomes. Additionally, because income may be tied to volatility monetization, changes in volatility regimes may affect the terms available on new issuance within the fund over time.

Swap, Counterparty, and Liquidity Risk: Because the ETF gains exposure through a portfolio of synthetic autocallables rather than direct note ownership, investors may face counterparty risk and potential liquidity constraints. The swap structure may also introduce additional considerations like financing costs and the potential for the swap’s value to diverge from the referenced index.

Market Path Dependency: Results depend on how markets move over time, not just endpoints. Volatility and drawdown timing may influence outcomes unpredictably.

Income Variability: Distributions are conditional. Periods below observation thresholds may produce reduced or no income.

Downside Exposure: Significant drawdowns may result in principal loss. If the reference index breaches the maturity barrier, losses may occur in proportion to the index decline, and principal barriers do not eliminate this risk.

Reinvestment Considerations: Frequent autocalls may require reinvestment when terms are less attractive.